Retirement Planning

Retirement is not a single event. It is a new phase of life that requires a clear strategy for income, taxes, investments, and long-term decision-making.

Our process focuses on long-term financial planning, using objective analysis and advanced financial planning software to create a retirement roadmap you can follow with confidence. The result is a written financial plan that connects your goals with the resources you have and the choices you can control.

A Retirement Roadmap Built Around Your Life

A strong retirement roadmap starts with clarity. We work with you to define the retirement you want, then build a plan that coordinates the moving parts that matter most.

Your written financial plan may include:

- A retirement income plan that maps out where income will come from year by year

- Investment and retirement management guidance that fits your risk comfort and timeline

- Required minimum distribution planning and account withdrawal sequencing

- Tax-aware planning considerations and coordination with your outside professionals

- Contingency planning for healthcare costs, market volatility, and major life changes

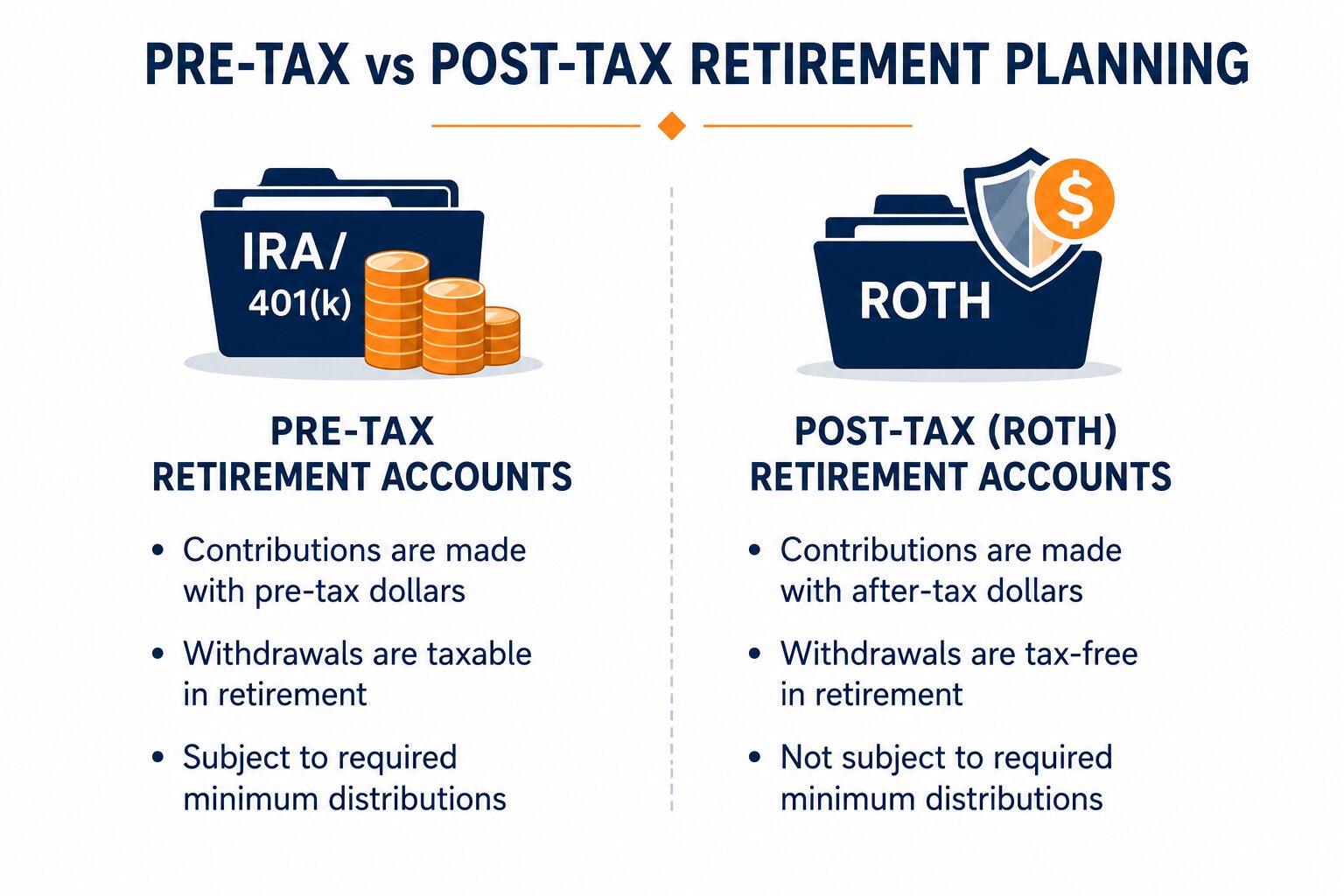

Pre-Tax vs. Post-Tax Retirement Planning

A well-designed retirement strategy should not depend on a single type of account. Instead, it should incorporate both pre-tax and post-tax retirement assets to create greater flexibility, control, and long-term tax efficiency.

Many clients come to us with a mix of traditional retirement accounts, such as 401(k)s and IRAs, and Roth accounts, including Roth IRAs and Roth 401(k)s. Traditional accounts are funded with pre-tax dollars, which means distributions are generally taxable in retirement. Roth accounts are funded with after-tax dollars, allowing qualified withdrawals to be received tax-free.

The real value lies in how these accounts work together.

By strategically coordinating withdrawals from different account types, we help clients manage taxable income, maintain greater control over their tax bracket, and create a more efficient retirement income strategy over time. This approach, often referred to as tax diversification, can provide meaningful flexibility throughout retirement.

Our planning process helps determine:

- When to withdraw from traditional versus Roth accounts

- How to manage income within targeted tax ranges

- How to coordinate distributions with Social Security and pension income

- How to reduce the long-term impact of required minimum distributions (RMDs)

The result is a retirement income strategy designed not only to support your lifestyle, but to help preserve more of what you have worked to build.

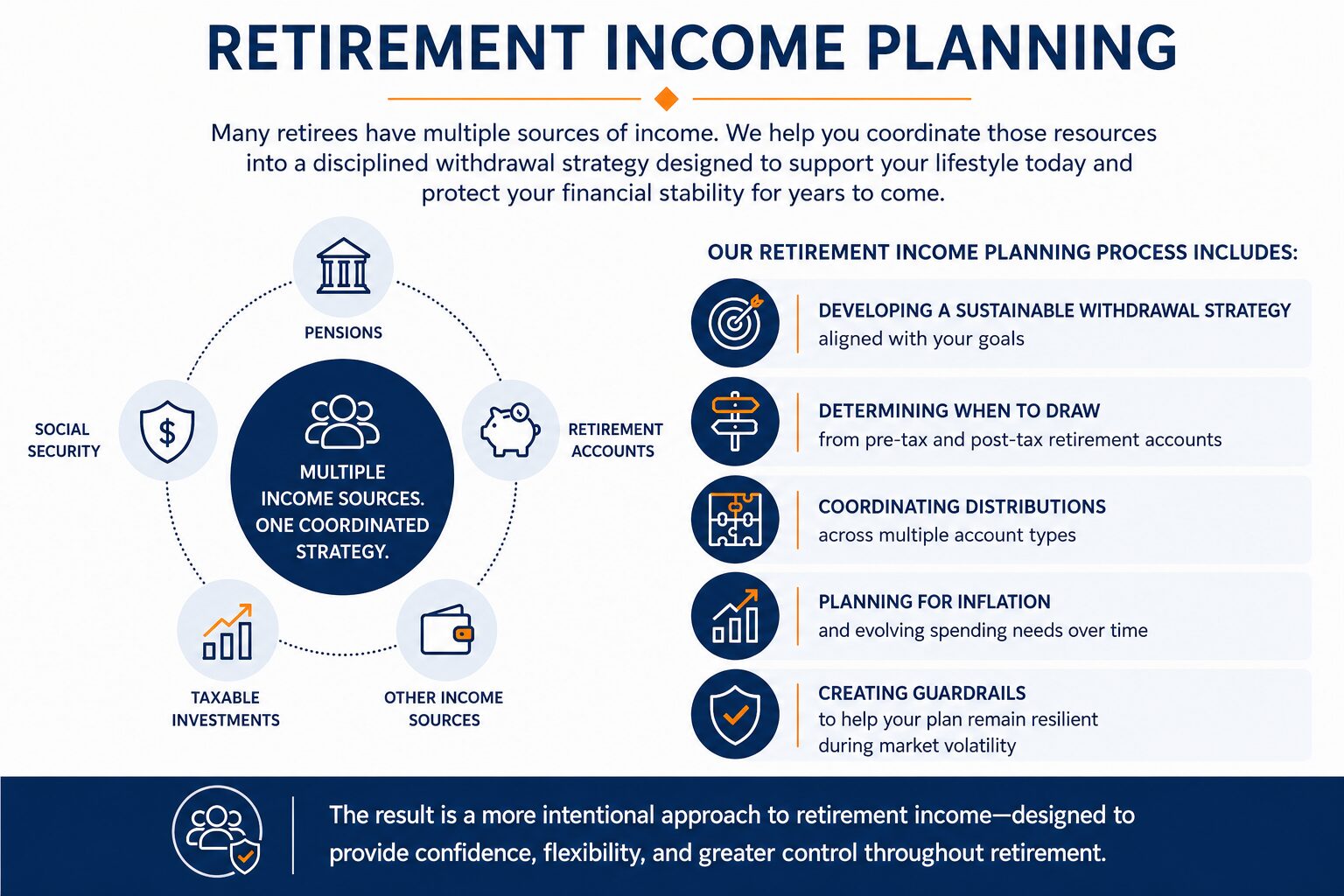

Retirement Income Planning

Many retirees have multiple sources of income, but without a coordinated strategy, those resources may not be used as efficiently as they could be. We help clients develop a retirement income plan that integrates pensions, Social Security, retirement accounts, and taxable investments into a disciplined withdrawal strategy designed to support both lifestyle and long-term financial stability.

Our retirement income planning process includes:

- Developing a sustainable withdrawal strategy aligned with your goals

- Determining when to draw from pre-tax and post-tax retirement accounts

- Coordinating distributions across multiple account types

- Planning for inflation and evolving spending needs over time

- Creating guardrails to help your plan remain resilient during market volatility

The result is a more intentional approach to retirement income, designed to provide confidence, flexibility, and greater control throughout retirement.

Pension Decisions and Payout Options

Employer pensions are less common than they used to be, but for retirees who have them, choosing a payout option can be a major decision. We help you understand how each option fits your household goals and risk tolerance.

Pension planning includes:

- Comparing lump sum vs. income options

- Evaluating survivor benefit choices

- Stress testing how each option affects long-term income in retirement

401(k) Consolidation and Retirement Account Strategy

It is common for retirees to have multiple 401(k) accounts from former employers. Managing several accounts can create confusion and complicate retirement management, especially when required minimum distributions begin.

We can help simplify your retirement accounts by reviewing across custodians, creating a consolidation strategy when appropriate, coordinating rollover decisions, and planning for required minimum distributions and future cash flow.

Retirement Management That Adapts Over Time

Retirement management is ongoing. Markets change. Healthcare needs change. Family priorities change. A good retirement plan is designed to evolve.

We review and adjust your plan to help you:

- Stay aligned with your income goals

- Rebalance and manage risk as circumstances change

- Update your retirement roadmap when life events occur

- Track progress against your written financial plan

Using Financial Planning Software to Build Clarity

Retirement planning is most effective when it is based on data and realistic scenarios. We use advanced financial planning software to model variables like Social Security timing, pension options, withdrawal strategies, market performance ranges, taxes, and longevity assumptions. This helps translate complex decisions into a plan you can understand and act on.

Reach out to us today to schedule a conversation with one of our trusted advisors.

Planning Your Retirement

Employer pension plans are not as common as they once were. At Integrated Capital Management we educate our clients on their individual pension options for maximum payout.

Situation

David is Vice President of Sales of a public utility company and is fortunate to have a pension through his employer. He is currently evaluating the four pension options offered to him – three are income option plans and the fourth is a lump sum payout. He has asked Integrated Capital Management for guidance on which plan is best for him and his family. His goal is to retire within two years. He wants to elect the best pension option for his situation.

Solution

David’s Integrated Capital Management advisor reviewed his goals and pension options. Through a comprehensive financial planning analysis, a lump sum benefit was determined to be in David’s best interest. Based on his personal situation, this option was more beneficial to his family’s future financial stability.

For illustration purposes only. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy recommended will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. ICM and its affiliates do not provide tax, legal or accounting advice. Any information presented here is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

The average corporate employee has three 401(k) accounts that still reside with former employers. At Integrated Capital Management we see many employees nearing retirement who have not consolidated their 401(k) plans into one account.

Situation

Mary was referred to Integrated Capital Management after she had retired with three 401(k) accounts that were invested with her former employers. She was overwhelmed with managing the three accounts and the required minimum distributions.

Solution

Her advisor recommended to combine the three 401(k) accounts into one retirement account. This eased Mary’s concerns about managing so many accounts and streamlined the sources of her retirement income. The strategy simplified her future required minimum distributions and enabled the efficient management of her retirement accounts.

For illustration purposes only. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy recommended will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. ICM and its affiliates do not provide tax, legal or accounting advice. Any information presented here is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Most retirees are concerned about creating sustainable retirement income. Between Social Security, pensions and 401(k) / 403(b) accounts, retirees have multiple options for meeting their retirement needs, but many have no plan to maximize the income from these sources.

Situation

Steven was nearing retirement when he reached out to Integrated Capital Management. He needed help on how to structure his income from his old 401(k) accounts, pension and Social Security. His concern was that these sources would not be sufficient to enable him to retire comfortably.

Solution

The advisor worked with Steven to develop a retirement income plan that would also allow his family to take an annual vacation together, which was a lifelong goal for he and his wife. The long-term strategy took into consideration future variables such as the correct age to take Social Security, required minimum distributions from his 401(k) plans and taxes. With this strategy in place, Steven is confident that he and his family will have the income needed to enjoy the future.

For illustration purposes only. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy recommended will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. ICM and its affiliates do not provide tax, legal or accounting advice. Any information presented here is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

One of the most common questions we get at Integrated Capital Management is when to start taking Social Security benefits. Most retirees can begin taking Social Security benefits at age 62, however for each year you delay your income the monthly payment increases by 8%. Over your expected lifetime, taking an early Social Security check can cost you hundreds of thousands of dollars.

Situation

Patrick is 62 years old and has been an Integrated Capital Management client for 5 years. He would like to retire at age 65 and is considering taking his Social Security income check at that time. Patrick has several retirement and after-tax investment accounts that Integrated Capital Management manages that are possible sources of retirement income. He wants to evaluate the optimal income strategy from his investment accounts and his Social Security benefits.

Solution

Patrick and his Integrated Capital Management advisor built a financial plan that maximizes his income in retirement. The plan illustrates the benefit of Patrick waiting to take Social Security until age 70 while using his other investment accounts to generate income from age 65 to 70. This strategy ensures that he will not outlive his money while covering his family’s income needs. He is now confident that he can enjoy retirement as he had planned.

For illustration purposes only. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy recommended will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. ICM and its affiliates do not provide tax, legal or accounting advice. Any information presented here is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Frequently Asked Questions

Yes. We build written financial plans that serve as a retirement roadmap and help you make decisions with clarity.

Yes. Income in retirement planning is a core focus, including coordinating Social Security, pensions, retirement accounts, and taxable investments.

Yes. We model claiming strategies and coordinate Social Security timing with your broader retirement plan.

Yes. We help retirees simplify accounts, plan rollovers when appropriate, and build strategies for required minimum distributions.